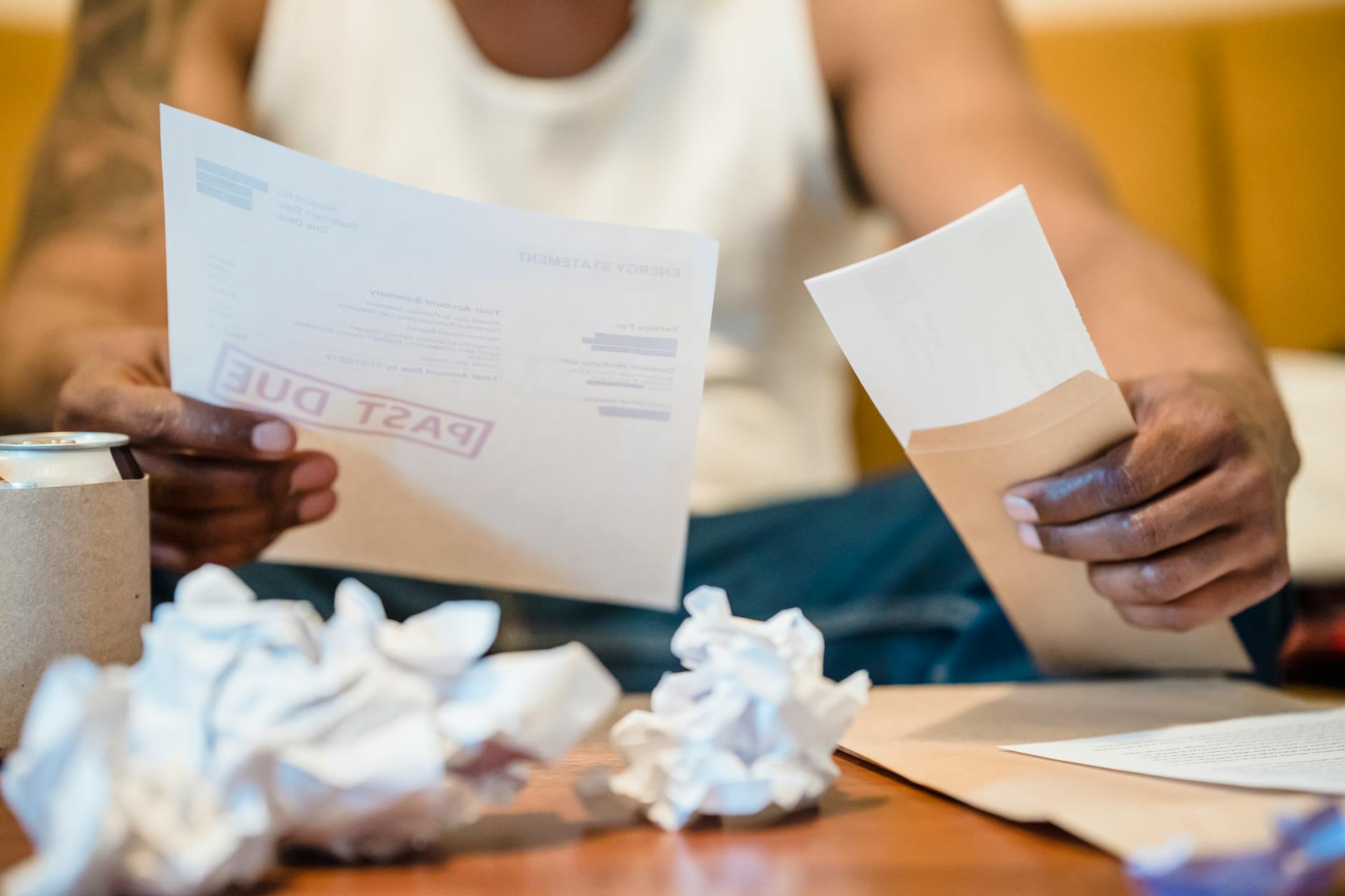

If you are behind on property taxes in New York, the clock is working against you. New York State law gives municipalities the authority to place a tax lien on your property and, eventually, move toward a tax foreclosure sale if the debt goes unpaid long enough. The good news is that Long Island homeowners have several real options to resolve delinquent property taxes before the situation spirals out of control – from official repayment programs to selling the home for cash and walking away debt-free.

How Property Tax Delinquency Works in New York

New York has some of the highest property tax rates in the entire country. According to the New York State Department of Taxation and Finance, the effective average property tax rate across the state hovers around 1.4%, but in Nassau and Suffolk Counties it can climb significantly higher. The average Nassau County homeowner pays well over $10,000 per year in property taxes, and Suffolk County is not far behind.

When you miss a property tax payment, penalties and interest start accruing almost immediately. In most Long Island municipalities, unpaid taxes become “delinquent” after the due date passes, and a monthly interest penalty – often between 1% and 1.5% per month – is tacked onto the balance. The longer you wait, the bigger the hole gets.

Eventually, if taxes remain unpaid, the county has the authority to begin the tax foreclosure process. In New York, this is governed by Article 11 of the Real Property Tax Law, which allows counties to foreclose on properties with delinquent taxes. This is separate from mortgage foreclosure, and it can happen even if you own your home outright with no mortgage.

The Tax Lien Process on Long Island

Understanding exactly how the tax lien and foreclosure process works in Nassau and Suffolk Counties will help you know how much time you actually have – and where the real deadlines are.

In Nassau County, the county sells tax liens to third-party investors at an annual lien sale. Once a lien is purchased by an investor, that investor earns interest on the debt (New York State law caps the rate at 18% annually for residential properties under certain circumstances). If the lien is not redeemed within the legally specified redemption period, the lienholder can eventually begin foreclosure proceedings.

In Suffolk County, the process is handled somewhat differently. Individual towns within Suffolk, including Babylon, Islip, and Brookhaven, handle their own tax collection and enforcement. Suffolk County conducts an annual tax lien sale as well, and properties with long-standing delinquencies can be moved toward in-rem foreclosure proceedings, where the county itself takes title to the property.

The key point for Long Island homeowners is this: once a tax lien is sold to a third-party investor, you are no longer just dealing with the county. You are dealing with an investor whose primary goal is to collect the debt plus maximum interest. Redeeming that lien requires paying not just the original tax debt but all accrued interest, penalties, and administrative costs.

By the Numbers: Property Tax Delinquency on Long Island

- $10,000+: Average annual property tax bill in Nassau County, one of the highest in the United States

- 1%-1.5% per month: Typical interest and penalty rate on delinquent property taxes in New York municipalities

- 18% annually: Maximum interest rate a tax lien purchaser can charge on residential property in New York State under current law

- 1-2 years: Typical timeline before a tax lien sale occurs after initial delinquency in Nassau and Suffolk Counties

- 2-5 years: Approximate total timeline from first missed payment to completed tax foreclosure in New York, depending on the municipality and investor actions

- 45-60 days: Typical time to close a home sale with a traditional realtor, compared to 7-14 days with a cash buyer

Repayment Plans and Hardship Programs Available in New York

If you want to keep your home and are simply going through a rough financial patch, the first place to turn is your local tax authority. Both Nassau County and the individual towns within Suffolk County offer structured repayment plans for homeowners who are behind on property taxes.

Nassau County Delinquent Tax Installment Program

Nassau County has historically offered installment payment agreements that allow homeowners to pay off delinquent taxes over time while keeping their home out of the lien sale. These programs typically require a down payment and monthly installments, and you must stay current on future tax bills while repaying past debt. Contact the Nassau County Department of Assessment or the Nassau County Treasurer’s office directly to ask about current eligibility requirements.

Suffolk County Town Payment Plans

Each of the ten towns in Suffolk County administers its own tax collection. Towns like Babylon, Islip, Huntington, Brookhaven, and Smithtown each have their own procedures for setting up payment agreements. Call your town’s Tax Receiver office to ask about a delinquency repayment plan before your taxes are included in a lien sale.

New York State’s STAR and Enhanced STAR Programs

If you are not already enrolled in the School Tax Relief (STAR) program, doing so can meaningfully reduce your annual property tax burden going forward. The Basic STAR exemption provides a reduction on school taxes for primary residences, while the Enhanced STAR program offers larger savings for homeowners who are 65 or older and meet income requirements. While this does not erase existing debt, it lowers future bills and frees up cash to chip away at what you owe.

Senior Citizen and Disability Exemptions

New York State also offers property tax exemptions for qualifying senior citizens and homeowners with disabilities. If you are 65 or older and meet income thresholds set by your local municipality, you may qualify for an exemption that reduces your assessed value by 50% or more. Veterans’ exemptions are also available. Applying for these exemptions reduces your ongoing tax liability and can make staying current much more manageable going forward.

Exemptions That Can Reduce Your Property Tax Bill

Many Long Island homeowners do not realize they may be eligible for property tax exemptions they have never applied for. These exemptions reduce the assessed value of your property, which directly lowers your tax bill. Even if you are already behind, applying for an exemption going forward reduces how much you will owe in future years.

Common exemptions available in Nassau and Suffolk Counties include the Basic and Enhanced STAR exemptions mentioned above, senior citizen exemptions (up to 50% reduction in assessed value for qualifying seniors), Veterans exemptions for honorably discharged veterans, Cold War Veterans exemptions, exemptions for persons with disabilities, and exemptions for volunteer firefighters and ambulance workers.

Visit your local assessor’s office or the New York State Department of Taxation and Finance website to check eligibility and deadlines. In most municipalities, exemption applications are due in early spring for the following tax year.

If you believe your property has been over-assessed – meaning the taxable value is higher than your home is actually worth – you also have the right to grieve your assessment. Filing a tax grievance with your local Assessment Review Commission can result in a lower assessed value and a lower tax bill going forward. Many homeowners on Long Island successfully reduce their taxes this way each year.

Selling Your House to Resolve Tax Debt

For some Long Island homeowners, the math simply does not work out in favor of keeping the property. If you are behind on property taxes by tens of thousands of dollars, carrying a mortgage you are struggling to afford, and dealing with a home that needs significant repairs on top of everything else, selling may be the smartest and cleanest path forward.

Selling your home while behind on property taxes is absolutely possible. At closing, all outstanding liens including delinquent property taxes, any tax lien held by a third-party investor, and any mortgage balance are paid off from the sale proceeds before you receive your net equity. This means you do not need to come up with cash upfront to clear the tax debt – the buyer’s funds handle it at the closing table.

If you have built up equity in your Long Island home over the years, a sale can wipe out your tax debt completely and put cash in your pocket, giving you a genuine fresh start. Even if your equity is thin, a sale can help you avoid a tax foreclosure judgment that would destroy your credit and leave you with nothing.

For homeowners in this situation, our guide on selling your house fast on Long Island walks through why speed matters when you are carrying mounting debt. You can also explore who Square One Home Buyers helps to see if your situation fits the profile of homeowners we work with every day.

Cash Sale vs. Traditional Sale When Behind on Property Taxes

When time and financial pressure are working against you, the method of sale matters a great deal. Here is a direct comparison of your two main options:

| Factor | Traditional Realtor Sale | Cash Buyer (Square One) |

|---|---|---|

| Time to close | 45-90 days average | 7-14 days |

| Repairs required | Usually yes, for market value | None – sold as-is |

| Realtor commission | 5%-6% of sale price | None |

| Seller closing costs | 2%-4% of sale price | None paid by seller |

| Risk of deal falling through | High (financing, inspection) | Very low (cash, no contingencies) |

| Tax lien payoff handled at closing | Yes, but delays possible | Yes, handled cleanly and quickly |

| Suitable if taxes sold to lienholder | Possible but complicated | Yes, we handle the complexity |

As you can see, a traditional sale through a realtor is not necessarily wrong, but it carries risks that can be dangerous when you are racing against a tax foreclosure deadline or a lienholder’s redemption deadline. If the buyer’s financing falls through three weeks before closing, you are back to square one with the clock still ticking.

A cash sale eliminates that uncertainty. You know the closing date in advance, there are no financing contingencies, and the title company handles paying off the delinquent tax debt directly from the closing proceeds. You can also learn more about the pros and cons of selling to a cash buyer before making your decision.

How to Sell Your House for Cash to Pay Off Property Taxes: A Step-by-Step Guide

If you have decided that selling is your best path forward, here is exactly how the process works with a cash home buyer like Square One Home Buyers:

- Contact us and share your property details. You can submit your property information online or call us directly. Tell us about the home, its condition, and your situation. There is no obligation and no judgment – we work with homeowners in all kinds of circumstances every day.

- Receive your no-obligation cash offer. We will review your property and typically present a fair cash offer within 24-48 hours. Our offer accounts for the home’s current condition, so there is no need to make any repairs or improvements before selling.

- Review and accept the offer. Take your time reviewing the offer. We are happy to walk you through every detail and answer any questions. There is never any pressure to accept.

- Open title and coordinate the payoff. Once you accept, we open title with a local title company. The title search will identify all outstanding liens, including delinquent property taxes and any tax lien held by a third-party investor. The title company will get payoff figures for everything owed.

- Choose your closing date. We work around your schedule. Most homeowners we work with close within 7-14 days, but if you need a little more time to make arrangements, we can accommodate that too.

- Close and receive your funds. At closing, all liens including delinquent property taxes are paid directly from the sale proceeds. You receive your net equity, and the tax debt is gone. You walk away with a clean slate.

If you want to understand the typical timeline in more detail, our post on how long it takes to sell a house for cash on Long Island breaks down each stage of the process. And if you are also dealing with a mortgage on top of the tax debt, you may find it helpful to read about selling your house when you are behind on your mortgage as well.

Frequently Asked Questions

How long before New York can foreclose on my home for unpaid property taxes?

In New York, the property tax foreclosure timeline varies by county and municipality, but in general, it takes between two and five years from the first missed payment before a completed foreclosure judgment removes your ownership rights. However, once your taxes are sold to a third-party lienholder, that investor can pursue foreclosure more aggressively within a shorter timeframe depending on the redemption period specified under New York law. Acting quickly – well before a foreclosure proceeding is filed – gives you the most options.

Can I sell my house if I owe back property taxes in New York?

Yes, you can sell your house even if you owe back property taxes in New York. The delinquent tax debt, including any penalties, interest, and tax liens held by investors, is paid off at closing from the sale proceeds before you receive your net equity. You do not need to pay off the taxes before listing or accepting an offer. A cash buyer can handle this process quickly and cleanly, typically within 7-14 days.

What happens if I just ignore my property tax debt in New York?

Ignoring delinquent property taxes in New York leads to escalating penalties and interest, a tax lien sale where your debt is sold to a third-party investor, and eventually a tax foreclosure proceeding where you can lose your home entirely – potentially without receiving any of your equity. Once a foreclosure judgment is entered in New York, the homeowner can lose all rights to the property and any remaining equity. This outcome is avoidable if you take action early by setting up a payment plan, applying for exemptions, or selling the property.

Are there any free programs to help Long Island homeowners with delinquent property taxes?

Yes, several free resources exist. The New York State STAR and Enhanced STAR programs reduce school tax burdens for qualifying homeowners at no cost. Senior citizen, veteran, and disability exemptions can significantly reduce your ongoing tax liability. Nassau and Suffolk County towns offer installment repayment plans that let you pay off delinquent taxes over time. Additionally, HUD-approved housing counselors are available at no charge to help homeowners explore all available options when facing tax delinquency.

Will selling my house for cash hurt my credit if I am behind on property taxes?

Selling your house for cash when you are behind on property taxes typically has a neutral to positive effect on your credit compared to the alternatives. A tax foreclosure judgment or a third-party lienholder pursuing collections can damage your credit significantly. A voluntary sale that pays off all outstanding debts at closing resolves the liens cleanly and prevents negative credit reporting associated with foreclosure. After the sale, your credit reflects a resolved debt rather than an ongoing delinquency or foreclosure action.

Get a Fair Cash Offer and Put Your Property Tax Debt Behind You

If you are behind on property taxes on Long Island and need to find a fast, reliable solution, Square One Home Buyers can close in as little as 7-14 days, pay off all tax liens at closing, and put cash in your hands – with no repairs, no commissions, and no surprises.